WE’RE HERE TO HELP YOU

Information and resources on mortgage rates and plans

Austin Capital Mortgage wants to help you succeed, so our experts have compiled resources addressing mortgage types, rates, services, solutions, and calculations. Whether you’re looking for inspiration, trying to understand how to purchase a home, or evaluating a refinance, we have content that can help you.

Are you a homeowner needing extra cash? Or perhaps you want to take advantage of the low interest rates? In either case, a cash-out refinance might be the solution you're looking for. A cash-out refi allows you to tap into your home's equity and receive a lump sum of money, which can be used for various purposes. In this comprehensive guide, we will explore the concept of cash-out refinancing, understand when it makes sense to pursue this option and learn how to get started.

When it comes to home improvements, homeowners are often looking for projects that not only enhance the aesthetics and functionality of their homes but also provide a good return on investment (ROI). Home improvements that yield the highest return are the ones that not only add value to your property but also attract potential buyers if you plan to sell in the future. In this article, we will explore various home improvement ideas that can significantly boost your home's value. So, let's dive in and discover the best ways to increase the value of your home!

Are you looking to turn your Airbnb rental into a cash cow? If you're a property owner or a savvy investor, maximizing your rental income on Airbnb can be a game-changer. In this article, we will explore proven strategies and expert tips on how to have an Airbnb cash cow. From optimizing your listing to delivering exceptional guest experiences, we will cover everything you need to know to boost your rental income and achieve long-term success on Airbnb.

Are you looking to maximize the occupancy and return on investment (ROI) of your short-term rentals? Look no further! In this comprehensive guide, we will provide you with valuable tips and strategies to help you achieve optimal results with your rental properties. Whether you're a seasoned host or just starting out in the short-term rental market, these tips will give you the edge you need to succeed. So let's dive in and unlock the secrets to maximizing occupancy and ROI!

In the competitive world of short-term rentals, attracting guests and maximizing occupancy is crucial for success. One effective way to achieve this is through interior design. A well-designed space can create a lasting impression on guests, making them more likely to choose your rental over others. This article explores how interior design can boost occupancy on your short-term rental, providing practical tips and insights to help you create an inviting and desirable space.

Welcome to our comprehensive guide on achieving competitive mortgage rates in 2023. At Austin Capital Mortgage, we understand the importance of finding the best mortgage rates to suit your financial goals. This article will provide valuable insights, tips, and strategies to help you secure a favorable mortgage rate in today's market.

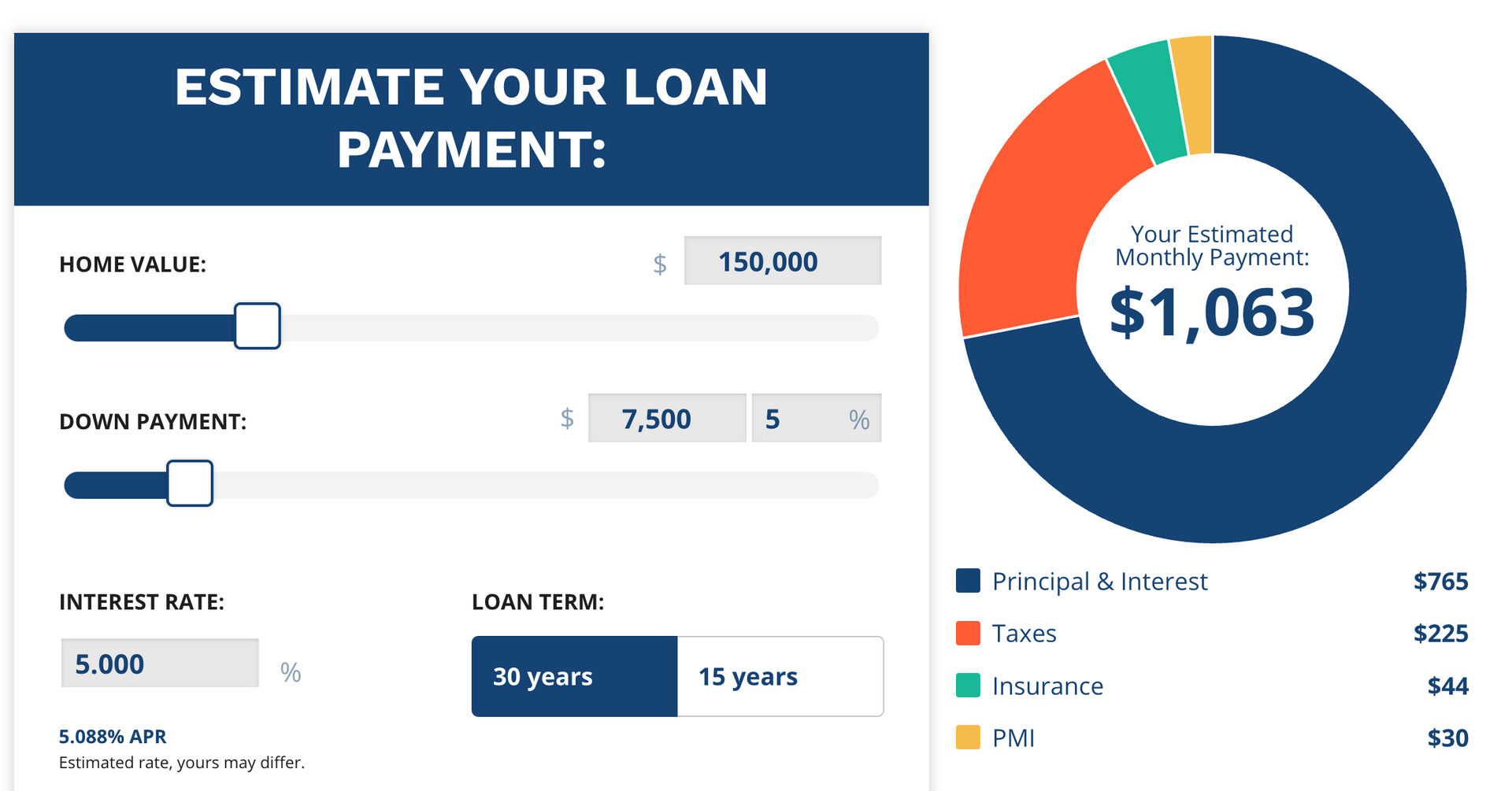

Buying a home is one of the biggest investments you will make in your lifetime. And with it comes the responsibility of paying a mortgage. While it can be daunting to think about the long-term financial commitment, there are ways to save money on your mortgage. One of the most useful tools available is a mortgage calculator. Using this tool, you can determine your monthly payments, how much interest you will pay over the life of your loan, and how much you can save by making extra payments. This article will explore some tips and tricks for saving money on your mortgage using a mortgage calculator. Whether you are a first-time homebuyer or a seasoned homeowner, this information will help you make informed financial decisions and potentially save you thousands of dollars over the life of your loan. So, let's get started!

Are you considering purchasing a home but struggling to save for a large down payment? Traditional mortgages typically require a substantial upfront payment, making it challenging for many aspiring homeowners to enter the market. However, a 1% down mortgage option offers a viable alternative. In this article, we'll explore the benefits of 1% down mortgages and provide valuable insights on how you can secure one.

Sign up for important updates and announcements.

Sign up to receive special offers from our team.