Texas Top Mortgage Lenders Since 1996

Texas Construction Loans: Flexible Financing for Builders & Investors

Shop Multiple Lenders. Get the Best Rates. Build with Confidence.

Financing a construction project isn’t as simple as a traditional mortgage.

High costs, unpredictable expenses, and strict lender requirements can slow you down.

At ACM, we help real estate investors, builders, and contractors in Texas find the right loan for their projects - without unnecessary delays or hidden fees.

5/5

Nature's Symphony

Texas' Top Mortgage Lenders Since 1996

Why Work with ACM as Your Mortgage Broker?

Unlike banks that offer limited loan products, we compare multiple lenders to find the best rates and terms for your project. Here’s how we help:

- Competitive Interest Rates: Get the best deal by shopping multiple lenders.

- Tailored Loan Options: Financing designed for investors, builders, and contractors.

- Manage Cash Flow with Staged Funding: Access funds as construction progresses.

- Lower Down Payment Options: Some programs require as little as 5% down.

- Guidance on Taxes & Loan Structure: Avoid tax pitfalls and optimize your investment.

- 100% Online Application: Apply from anywhere, anytime.

Construction Loans Made Easy

Whether you're starting from the ground up or making major renovations, our construction loans make it easy to finance your project from start to finish, covering everything from land purchase to final construction costs.

Worried about high upfront costs?

We connect you with lenders offering lower down payments and staged disbursements.

Not sure how loan terms impact taxes?

We help you structure financing to minimize your tax burdens.

Struggling with approval due to inconsistent income?

We work with lenders who understand investor and builder cash flow cycles.

Need financing for land plus construction?

We offer options that cover both land acquisition and building costs.

How to Get Approved for a Construction Loan in Texas?

As Texas' Top Mortgage Brokers, we shop all lenders to get you the best rates and terms for your loan.

Our team of in-house underwriters and top loan officers ensure you get the best possible deal without any delays.

1. Pre-Approval: Understand your borrowing power before you start.

2. Project Review: Submit your building plans and estimated costs.

3. Funding & Draws: Receive funds in stages as construction progresses.

4. Loan Conversion: Transition to a long-term mortgage once your project is complete.

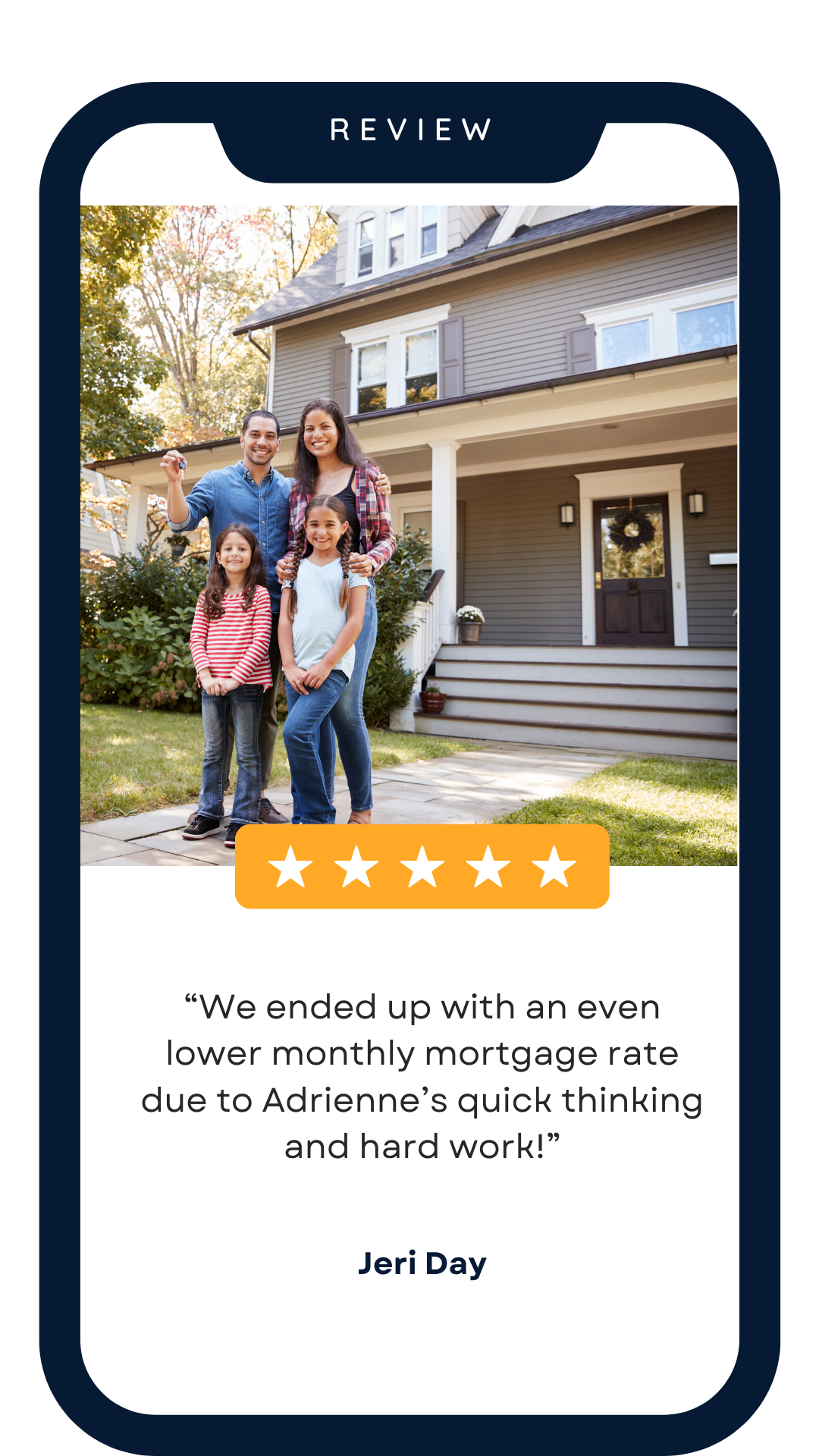

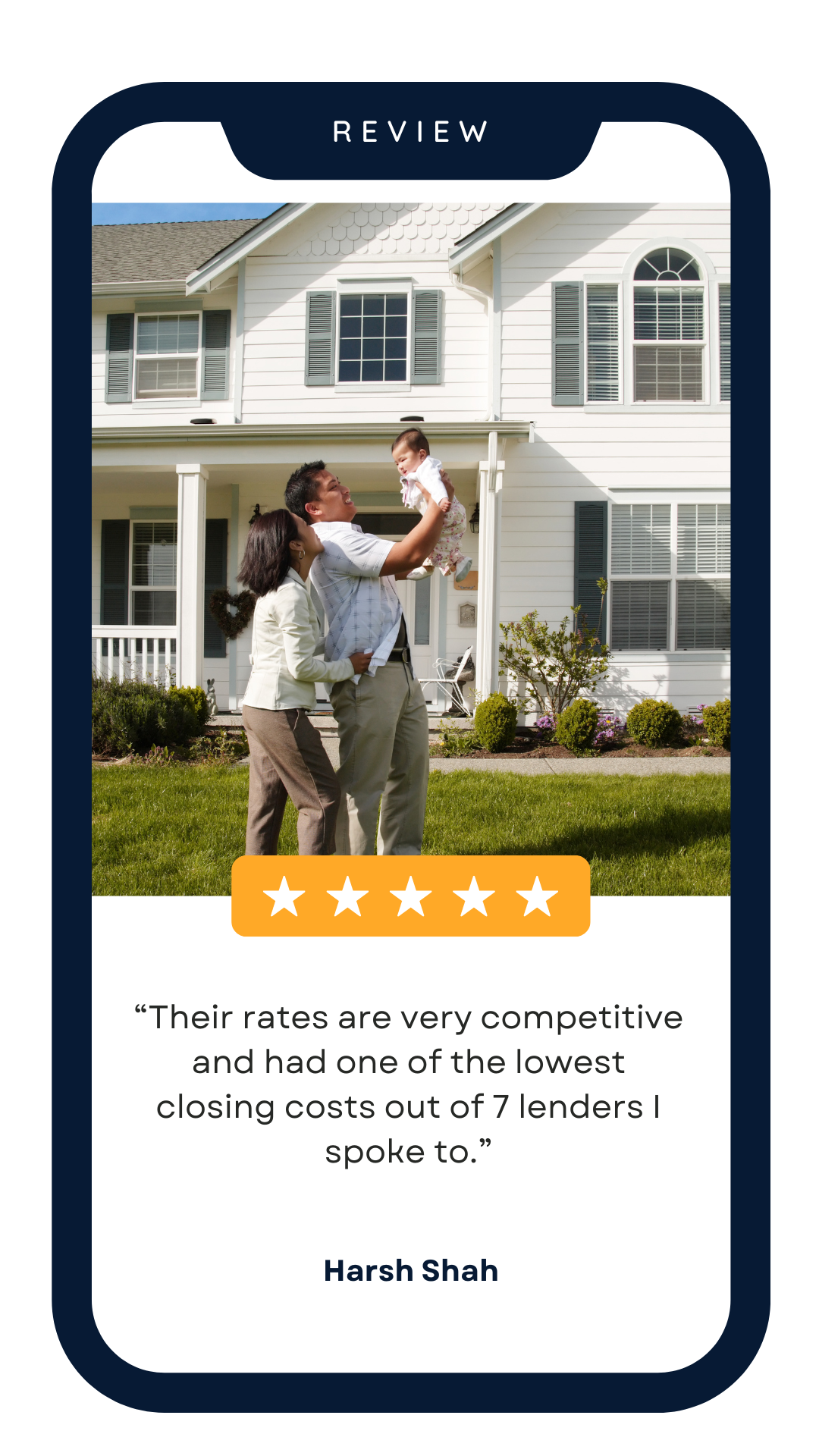

Hear What Our Clients Say About Us

As Texas' top rated mortgage lenders, we have a stellar reputation with an average rating of 5 Stars across all channels: Google, Yelp, Zillow, BBB and Facebook.

FAQs

Got a question? We’re here to help.